Liberty report: Hope for the premium on-trade

A new report on the premium on-trade from Liberty Wines, released today (5 February) and shared exclusively with Harpers, suggests that the only way to drive sales is to compete on quality.

The Liberty Wines Premium On-Trade Wine Report 2026 reveals that over the past year, wine sales by volume shrank 8% across the on-trade while value sales fell by 5% in the premium on-trade. Contrast this with the period between 2015 and 2019, when wine sales volumes shrank by 13%, but the premium on-trade grew by around 17% in terms of value. What went right over that four-year period? The premium on-trade convinced consumers to spend more money on better-quality wine, and they did. Now Liberty Wines, the source of all figures given here, thinks that approach should be repeated.

The Report’s argument is straightforward. To start, the causes of on-trade wine volume decline need to be assessed.

The first thing to note is that decline in on-trade wine volume performance is a long-term problem – something it is perhaps easy to lose sight of when considering the barrage of short-term challenges currently facing the on-trade.

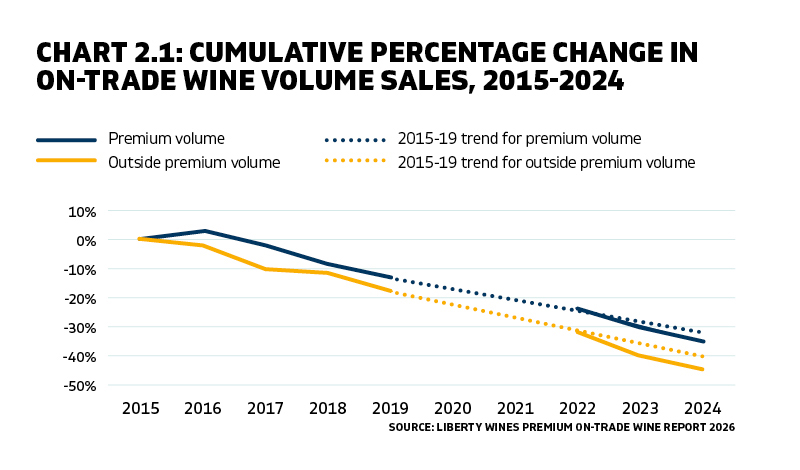

For a decade, wine volume has been falling year on year in the sector (as can be seen in Chart 2.1), meaning that the causes of the decline across 2015-2019 – when the premium on-trade grew – are likely to be the same as now. Driving this decline are two structural factors. The first, falling alcohol consumption per head (which has been shrinking since 2007), is partially offset by the growing adult population of the UK, which increased 6% from 2015-2023.

The second, much more significant, factor is consumers choosing to drink at home. This has had a huge impact on the on-trade – since 2016, the percentage of wine consumed in the sector fell from 20% to 13.2%.

The report indicates that had the wine market remained the same size over this period, the change in consumer behaviour would have implied a 33% drop in on-trade wine volume, explaining almost all the actual 35% decline at the premium end. (In the non-premium on-trade, volumes declined further, suggesting other factors at play there.)

While around two-thirds of the decline in wine volume can be explained by long-term factors, the short term also needs consideration and a powerful factor is the cost of living crisis, the major cause of the accelerated rate of decline visible on Chart 2.1 between 2022 and 2024. Over this period a 10% drop would have been expected, but in fact premium on-trade wine volume fell by 16%.

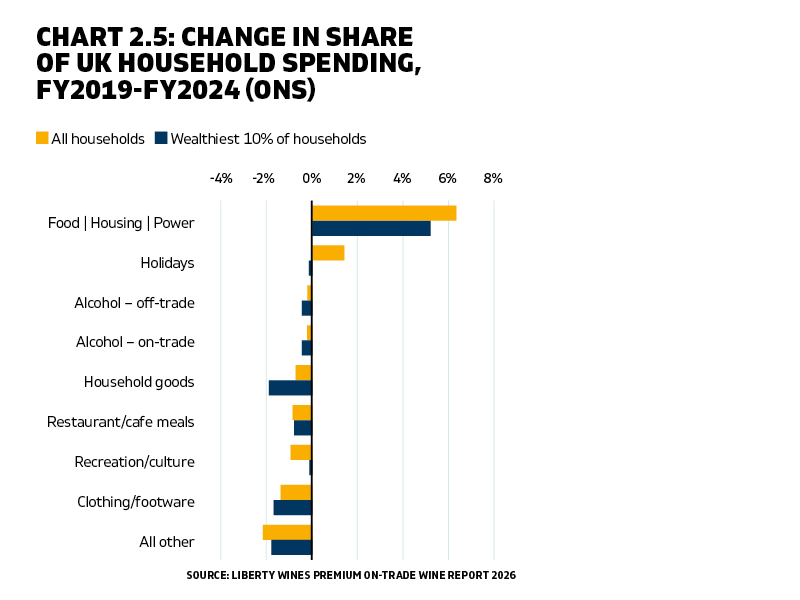

High inflation has eaten into disposable income, with the average household now spending over 6% more of their income on utilities and food than they did in 2019. Combined with the impact of lower consumer confidence this has altered spending habits in a damaging way.

At first glance, it looks as if spending in the on-trade has weathered this storm fairly well, with the share of household income spent in this way falling only by 0.2% across all households, or by 0.4% across the wealthiest 10% (see Chart 2.5). However, alcohol represents such a small proportion of household spending that such a reduction in share is a fall in actual spending of about 20%.

↓

Damaging effect

Additionally, consumers have more and more been visiting the premium on-trade with the intention of only having a drink, not eating out, which is especially damaging for wine sales as 40% of drinks sold in restaurants are wine, as opposed to only 17% of drinks sold in pubs and bars.

It is tempting to think that a surefire way to remain profitable under these conditions would be to cut costs – and with them quality. However, Liberty urges against this. The major reason for volume decline is consumers drinking more at home, so cutting back on quality simply brings the experience of the premium on-trade closer to the experience of sitting in their living room with a bottle of wine – giving them less reason to go out.

In some ways this is obvious from Chart 2.1, which shows non-premium on-trade wine volume has fallen even faster than the premium sector.

Further evidence of this is provided by the 2015-19 period. Over this time, average bottle spend rose by an impressive 35%, allowing the trade to grow despite declining volume. Average bottle price growth then slowed, first to 14% (2019-2022) and later to 7% (2022-2024), which, combined with accelerated volume decline, caused the sector to shrink by nearly 10%.

Liberty suggests there is a continued willingness to spend more on wine in the premium on-trade when compared to the wider sector, indicating that getting the consumer experience right is how to tackle selling wine.

Due to this, the report looks at which regions and grapes are currently performing well in the premium on-trade, as this provides a clue as to how to interest consumers and get them out of their homes.

Liberty found that consumer engagement with wine is in fact growing, with wine consumers in the premium on-trade becoming increasingly adventurous. Consequently, there has been significant growth in sales from countries outside the top 10 or which offer a “wealth” of indigenous grape varieties (see Charts 4.3 and 4.4).

This includes places such as Portugal and Italy, which were increasing their share of sales since before Covid, and Spain, which really began to increase its market share in the past year. Even in Argentina, where Malbec grew significantly, the grape accounts for less than half the country’s overall sales growth, pointing to high consumer interest in both known and lesser-known indigenous varieties.

Chart 4.4 tells the same story, with grapes outside the top 10 sellers increasing market share by nearly two percentage points, caused both by consumers trying the “new and exotic” and choosing from a broader range of grapes.

The premium on-trade is well placed to provide both breadth and quality of choice – after all, these traits are essentially what makes it ‘premium’. Consumer behaviour can be hard to shift, but if the sector can capitalise on its strengths, growth can follow.

↓

The report’s scope

Every year, Liberty Wines releases its Premium On-trade Wine Report, which looks at the performance of wine at the top end of the on-trade. While previous reports have analysed only the top 5% of outlets, this year the distributor has expanded its scope, focusing on the highest-quality 28%, accounting for 42% of all on-trade volume (and 49% of value).

Keywords:

Search

Digital Editions

56-58 Church Walk, Burgess Hill, West Sussex, RH15 9AN

Registered in England No. 6646125. VAT No. 938 4452 95