As alcohol lags behind on-trade recovery, where does the trade go from here?

The restaurant sector is showing some strong recovery after running the gauntlet for the past couple of years. However, alcohol’s future looks more tenuous, with the role of drinks – and the share of more expensive, premium products – becoming increasingly squeezed by ever-ratcheting living costs.

Already into the second week of November, the countdown to Christmas is on. There’s everything to play for. Though the staffing and cost of living clouds still hover, the prospect of the first Christmas in four years without the shadow of Covid restrictions means proprietors can finally pull out all the festive stops. Such freedom has been much missed, particularly during a period when the final six weeks of sales can – in good years – account for a hefty fifth, or even a quarter, of annual turnover.

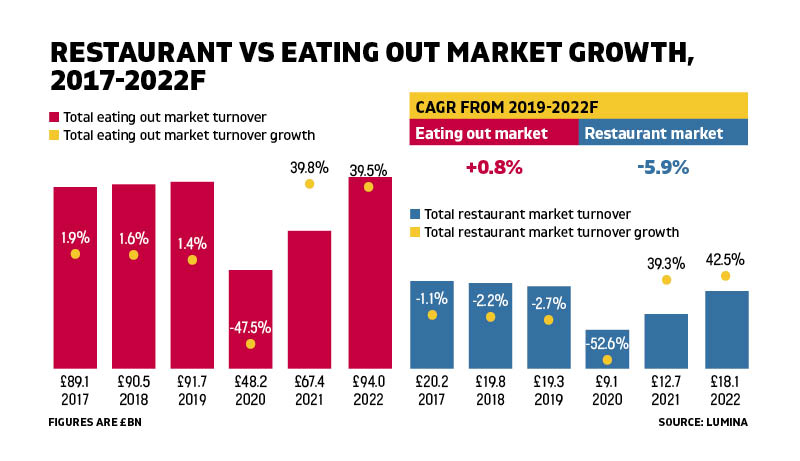

Encouragingly, the restaurant market has shown signs of some strong recovery over the past year. On-trade forecasts shared with Harpers from on-trade market analysts Lumina Intelligence, which tracks high-profile restaurant, bar and pub brands, show that the sector is expected to have regained the lion’s share of the value, which has been lost in the years since 2019, rising back up to £18.1bn by the year’s end (see graph). When the question turns to alcohol however – and the crucial role it plays in profits – the view becomes less clear and rosy. Could that recovery have been stronger – and quicker – if alcohol had played a bigger part?

When compared with the total eating out market, which includes a vast swathe of coffee and fast-food venues, the impact of alcohol declines is clear. Average spend at both lunch and dinner occasions have been on the wane, down 20% and 12% year on year (12 weeks to 2 September, 2022 versus 2021), with those falls driven by consumers – particularly younger ones – opting out of drinks purchases with food.

The figures, taken from the Lumina Restaurant Market Report, show how much the younger generation is moving away from what they consider expensive drinks.

Due to a combination of tightened belts and health-focused objectives, share of cocktails and spirits in the total alcohol category dropped 4.1ppt and 1.3ppt respectively in the 12 weeks to 2 September, as 18 to 34-year-olds opted for less expensive drinks or opted out altogether. (Food-only occasions increased share during this 12 week period, while both combined food & drink occasions and drink-only occasions suffered declines.)

The analysis of Lumina Intelligence, that “younger consumers are the most affected by the financial uncertainty” and that this is reflected in the number of drinks consumed on average, including wine and cocktails, is now a familiar take.

Inflationary costs have been on the rise for some time. The temperature gauge of the general cost of living in the UK was being tracked by the media long before Covid. But it is a stark reality that, although younger demographics were – in years past – more willing to splash their discretionary spend, despite having less of it than older generations, with the decision of ‘eating or heating’ becoming this winter’s ultimatum, that line no longer holds.

Businesses have been on the attack, however. With average spend down and alcohol becoming a casualty of squeezed pockets everywhere, pubs, bars and restaurants have been expanding their chances of sales by bumping up portfolios.

Between June and September, restaurants and pubs’ alcoholic ranges grew by 1.4% and 6.5% respectively (Lumina Intelligence’s Menu Tracker report), in the justifiable hope that wider choice means the greater the likelihood of a drinks purchase with meals.

Now, clearly, is the time to lean into those things that make the Christmas run-up such a lucrative time of year. There is no bigger ‘experience’ than Christmas. With a nation starved of fun and with a negative news agenda weighing heavily, operators have the chance to capitalise. There is an abundant appetite for buzzy, added-value extras and premium drinks, if the quality offer is there and the messaging right. And if that’s in place, there’s no reason optimism shouldn’t follow – and glasses be at least half full this winter.

Keywords:

- years

- alcohol

- restaurant

- drinks

- food

- market

- year

- share

- weeks

- 12 weeks

- recovery

- expensive drinks

- strong recovery

- restaurant market

- younger ones

- particularly younger ones

- restaurant market report

- market report show

- health focused objectives

- expensive drinks due

Search

56-58 Church Walk, Burgess Hill, West Sussex, RH15 9AN

Registered in England No. 6646125. VAT No. 938 4452 95