Insights: Taxing times ahead

With the aim of providing clarity for the trade, James Bayley once again highlights what’s coming down the line.

The UK wine and spirit industry has found itself at the brink of yet more tax-induced hardships, with the Labour government continuing the trajectory set by previous administrations, having delivered a Budget that will raise non-draught alcohol duties by 3.65% from 1 February in line with the Retail Price Index (RPI). This will be in addition to the lifting of the temporary ‘easement’, granted in response to industry lobbying over the previous Conservative government’s scheme, which delayed the introduction of new, escalating tax rates by 0.5% increases in abv.

These decisions, labelled “catastrophic” and “counterproductive” by trade leaders, are expected to elevate prices for consumers, reduce tax receipts for the Treasury and hinder the growth of the UK’s wine sector. And this is coming on the back of what the WSTA has highlighted as a nearly £500m shortfall in alcohol duty receipts within the first half of the financial year following last year’s near-record tax rises on alcohol.

- Read more: Trade expresses disappointment over Budget

Unsurprisingly, the drinks trade, which is fully supported and driven by the WSTA, is continuing to lobby government in the hope of making that easement permanent.

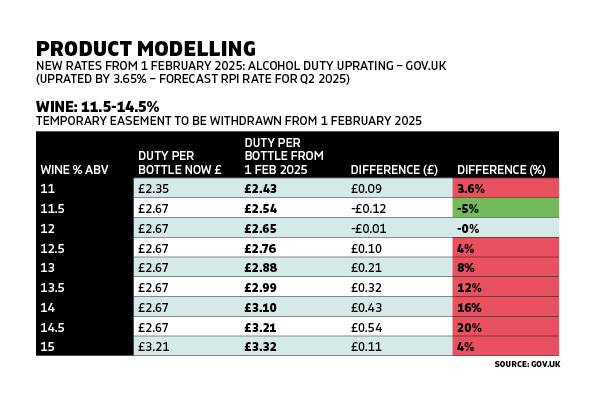

As it stands, starting from 1 February 2025, the tax system for wine will shift from a single, unified rate on wines in the 11.5-14.5% abv range to a graded structure based on alcohol content (see table). This change means that wine duty will now be calculated on each 0.5% abv increment. For example, a bottle at 14.5% abv will see its duty rate rise from £2.67 to £3.21, an increase of 20%. A bottle at 13.5% abv will see a 12% hike, with its duty rising to £2.99.

This incremental taxation is a departure from the simpler system currently in place, which taxes wines within this range at a flat £2.67 rate.

In total, this move is expected to create 30 separate duty rates, which the WSTA argues will lead to price hikes and less choice for consumers.

Industry experts highlight that the change fails to consider the nuances of winemaking, where the alcohol content is subject to natural variations depending on factors like climate and growing conditions. Unlike other alcoholic beverages that can be produced to a precise alcohol level, wine producers have limited flexibility. As a result, they are now burdened with the need to manage inventory across a more complex taxation landscape, which may strain their operational costs and complicate compliance with HMRC regulations.

Following the budget, the WSTA’s Miles Beale described the current fiscal approach as “bewildering” given Labour’s stated manifesto commitment to economic growth. “We simply cannot understand why the government is talking about protecting income and simultaneously raising alcohol duty,” he said. By ending the so-called ‘easement’ – a temporary fixed tax rate on wines between 11.5% and 14.5% abv – and introducing up to 30 new duty levels, the government is adding “pointless cost and complexity” to an already strained industry.

With rising duties and a loss of the easement, wine retailers and pubs are likely to face new disruptions. Already, large wine retailers such as Majestic and The Wine Society have been warning their customer bases about potential price hikes. This foresight is driven by the knowledge that with these policy changes, product costs are expected to rise as early as February next year, creating challenges for retailers who rely on stable pricing to keep customer loyalty.

↓

Operational challenges

Additionally, the industry is bracing for significant operational hurdles, with businesses anticipating that the withdrawal of the easement will introduce price volatility, particularly for wines near the 11.5% abv threshold. Pubs, bars and restaurants, often stocked with wines from multiple suppliers, may face inventory management challenges as they navigate this complex pricing structure, leading to an inconsistent pricing experience for consumers.

This will affect wholesalers and distributors, too. For example, one of Harpers’ Top 10 Wholesalers has revealed it is considering switching to a rolling digital price list only, updated monthly, as the option to allow for new vintages of existing lines to be appropriately priced as they come into stock throughout the year. The additional workload was described as “onerous and really frustrating”.

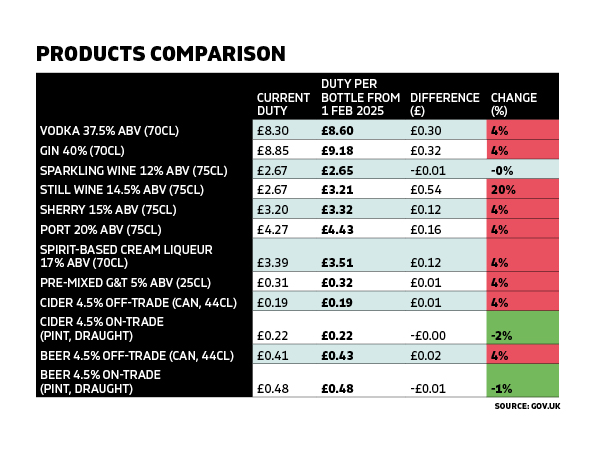

The changes to UK duty on wine from February 2025 will mark a stark contrast to EU practices. For a 13% abv wine, for instance, UK duty will stand at £2.87 plus VAT, nearly twice as much as the combined duty in the Netherlands, Belgium and Poland. France will levy a mere 3p duty on the same bottle. In Germany, Spain and several other EU states, the duty is zero. This disparity underlines the argument made by industry stakeholders, who question the benefits of this post-Brexit policy shift and argue that it will only drive up prices, impacting the UK’s competitiveness in the global wine market.

For consumers, this will translate to less choice on the shelves and higher prices, particularly for wines with higher alcohol content. According to Gavin Quinney of Château Bauduc, tax will soon account for 50% of the UK price of a £9 bottle of wine at 13.5% abv. For a £7 bottle at the same abv, this jumps to 60%. As consumers adjust to these changes, industry insiders anticipate a rise in sales of higher-alcohol wines in the lead-up to February, followed by a shift in demand to lower-priced wines.

The effect on smaller producers is equally concerning. Many winemakers who previously relied on the UK market for exports are expected to reconsider their strategies. In Australia, for example, where 90% of wine is shipped to the UK in bulk and bottled locally, the value of a 14.5% abv wine’s contents will be dwarfed by the duty alone. With duty at £3.21, the cost of the wine itself, averaging at 46p, becomes negligible in comparison. This discrepancy may force producers to re-evaluate the profitability of the UK market.

The industry’s frustration with these policies continues to spur calls for a reversal. The WSTA’s Beale has summarised the overall mood, calling for policies that prioritise economic development over complexity. Despite ongoing lobbying, there has been little indication the government is willing to reconsider its position.

As Quinney says, with UK duty on wine set to reach up to seven times the cost of the liquid itself, the situation appears bleak. Without a reversal or a meaningful intervention, the UK wine industry is set for turbulent times, with producers, retailers and consumers alike bearing the brunt of a policy misaligned with economic pragmatism.

Keywords:

Search

Digital Editions

56-58 Church Walk, Burgess Hill, West Sussex, RH15 9AN

Registered in England No. 6646125. VAT No. 938 4452 95