China to squeeze bulk supply of Australian red to critical levels over next 3-5 years

Bulk supply of some of Australia’s most popular grapes are due to significantly stall buyers have been warned, as a smaller 2018 harvest and the growing Chinese market leads demand to outstrip supply.

According to bulk supplier Austwine, this year’s vintage has slowed to a snail’s pace over the past two to three weeks after very hot conditions in January and February led to inhibited sugar accumulation and left growers waiting for grapes to ripen.

Clare Valley, Barossa, McLaren Vale Riverland and Mildura have all been affected, with widespread reports of average yields and slightly lower-than-expected crops.

As a result, last year’s record crop of 1.980mT has been forecasted to see a deficit of between 5% and 10%.

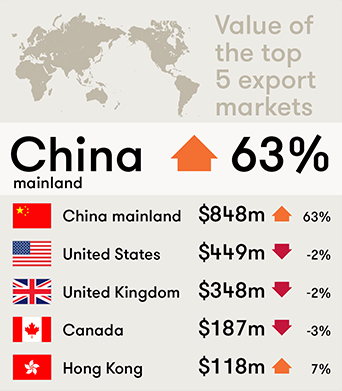

However, this is against a picture of staggering demand from China, where imports of Australian red jumped by 63% alone last year, from an already large base.

Austwine notes that commercial and entry level Shiraz, Cabernet Sauvignon and Merlot are now all “critically short” thanks to rocketing demand for red in China, which is now the biggest market for Australian wine by value.

Such growth means the country is now bigger than the US and the UK – Australian wine’s next two largest markets – combined.

The top five export markets for Australian wine for the 12 Months to December 2017 (The Australian Grape and Wine Authority (AGWA)

“During the past couple of years, producers of commercial level reds have probably experienced more enquiries than they have wine for,” said Jim Moularadellis, CEO at Austwine.

“It is certainly a very different supply situation across all commercial level red wines, compared to say, three years ago. The 2018 crop is unlikely to fully satisfy current demand at current prices, and any downside in the tonnes crushed will increase supply and pricing pressures as buyers try to get their share of wine.”

Premium reds and premium Chardonnay and Sauvignon Blanc have remained largely untouched by supply issues.

Volumes of entry level Sauvignon Blanc and Chardonnay are drastically down however, while being incorrectly assumed by most market players to be in abundant supply.

“One could easily count on one hand the number of inland wineries that have any substantial volumes of unallocated commercial Chardonnay from 2018 vintage,” added Moularadellis.

“I don’t think this is well understood by the market, including perhaps those few wineries that have unallocated commercial Chardonnay.”

Falling numbers of commercial Chardonnay crushed over the past three years has largely come about as a response to China’s low-level consumption of white wine and a subsequent push to remove Chardonnay vineyards in Oz over the past few years.

This is on the back of dwindling supplies of the grape globally.

South Africa’s recent drought and the well-publicised 2017 vintage shortfall in Europe have significantly impacted the availability of Chardonnay, with limited supply choice and price increases forecasted over the next few years.

Overall, supply increases of Australian wine are likely to be muted over the next three to five years, said Moularadellis, since there are currently only modest levels of planting activity and China will drive much of the demand for Australia’s wine going forward.

He said: “Should Chinese demand for Australian wine continue unabated, then bulk wine prices will rise in the absence of any significant new supply from Australia or alternative supply from other producing countries.

“A large 2018 European wine grape crop, plus the expectation of another large European crop in 2019 will be required to take the edge off the current outlook for increasing worldwide bulk wine prices. Australia’s wine fortunes are likely to be impacted by these events, together with what happens with crop levels in places such as Chile and South Africa.”

Keywords:

- wine

- UK

- US

- years

- wine prices

- Australian wine

- Chardonnay

- CEO

- demand

- Vineyards

- Australian

- supply

- over

- oz

- commercial

- level

- crop

- commercial chardonnay

- commercial level

- bulk wine prices

- grape globally

Search

56-58 Church Walk, Burgess Hill, West Sussex, RH15 9AN

Registered in England No. 6646125. VAT No. 938 4452 95