Big squeeze tipped for 2018 as lower volumes and tighter margins predicted

What is shaping up to be the smallest vintage in 50 years is predicted to cause a “dramatic decline in wine availability going into 2018”, with the lower-price tiers of the European industry expected to be the worst affected.

The first quarterly report form Rabobank following the disastrous 2017 vintage has forecast a “dramatic reduction” in supply of European wine next year, with rising bulk wine prices and tighter margins also having a knock-on effect globally.

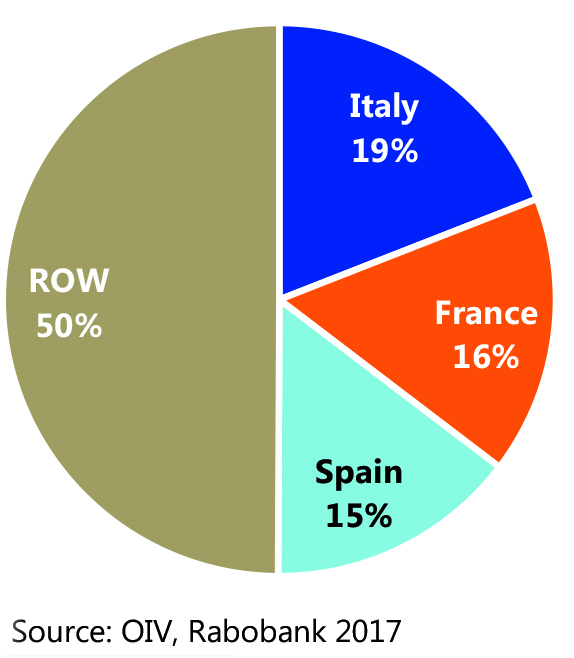

Declining availability and rising cost of grapes and bulk wine will be felt most acutely in Europe, the report said, where France, Italy and Spain, which make up 50% of global production, are suffering one of the worst crop shortages in decades.

Analysts suggest this could encourage premiumisation in developed markets, with brand owners able to leverage higher price points over a period of time. But in the short term, the price of grapes and bulk wine will rise, which “will not be enough to offset the decline in volumes” and will exacerbate already squeezed margins for growers.

“With grape and bulk wine prices rising, brand owners will inevitably need to pass on some price increases, as their thin gross margins will make it difficult for them to absorb the full price increase without passing some of that pain on to retailers and consumers,” said the report. “These price increases will weigh on consumption. Again, the lion’s share of this pain will be felt in Europe, but this will also have some knock-on effects for other regions.”

Balancing oversupply

Following the pre-harvest report, Rabobank strategist Stephen Rannekleiv told Harpers that vintage shortfalls in 2017 could help to balance out the oversupply which has been the norm in recent years, and it could be “healthier for brand-builders to have supply in balance or even a little tight”.

However, with the combined production from France, Italy and Spain expected to be down by approximately 15% in 2017 and poor harvests in Argentina squeezing wine inventories which were already tight at the beginning of 2017, supply issues are likely to make things difficult for winemakers across the board.

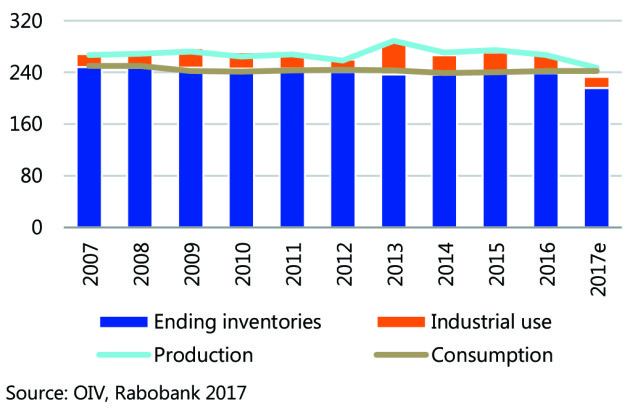

The report says: “The decline in production in these key European countries will mean that the global wine industry is going into 2018 with inventories that are likely to be at least 20 million hectolitres lower than they were going into 2017 – equivalent to nearly 8% of total global wine consumption. Wine available around the world will be at its lowest point in decades.”

Lower volumes and tighter margins set a challenging precedent for 2018. But there are possible gains to be had from a continued tightening of supply, including a greater consumer appreciation of the diversity and quality of what goes into their bottle. This is particularly relevant for the UK where consumers can get everything from New Zealand Pinot Noir to Washington Riesling at the drop of a hat – and all for under £6.

Things could be about to change.

Keywords:

Search

56-58 Church Walk, Burgess Hill, West Sussex, RH15 9AN

Registered in England No. 6646125. VAT No. 938 4452 95